Forget the headline number. The press releases will tell you that global venture funding is on track for a $75 billion quarter. They’ll call it “stabilizing.” They’ll talk about “a return to fundamentals.” Don't buy it. That’s the corporate spin. The real story, the one happening in pitch meetings from Sand Hill Road to Berlin, is a brutal, frantic rotation of capital unseen since the dot-com crash.

The money isn't just seeking safety. It's fleeing an entire thesis. For a decade, the VC playbook was simple: find a software that could scale to millions of users at near-zero marginal cost. The AI boom of 2023-2024 was the apotheosis of that strategy. Now, it’s a liability.

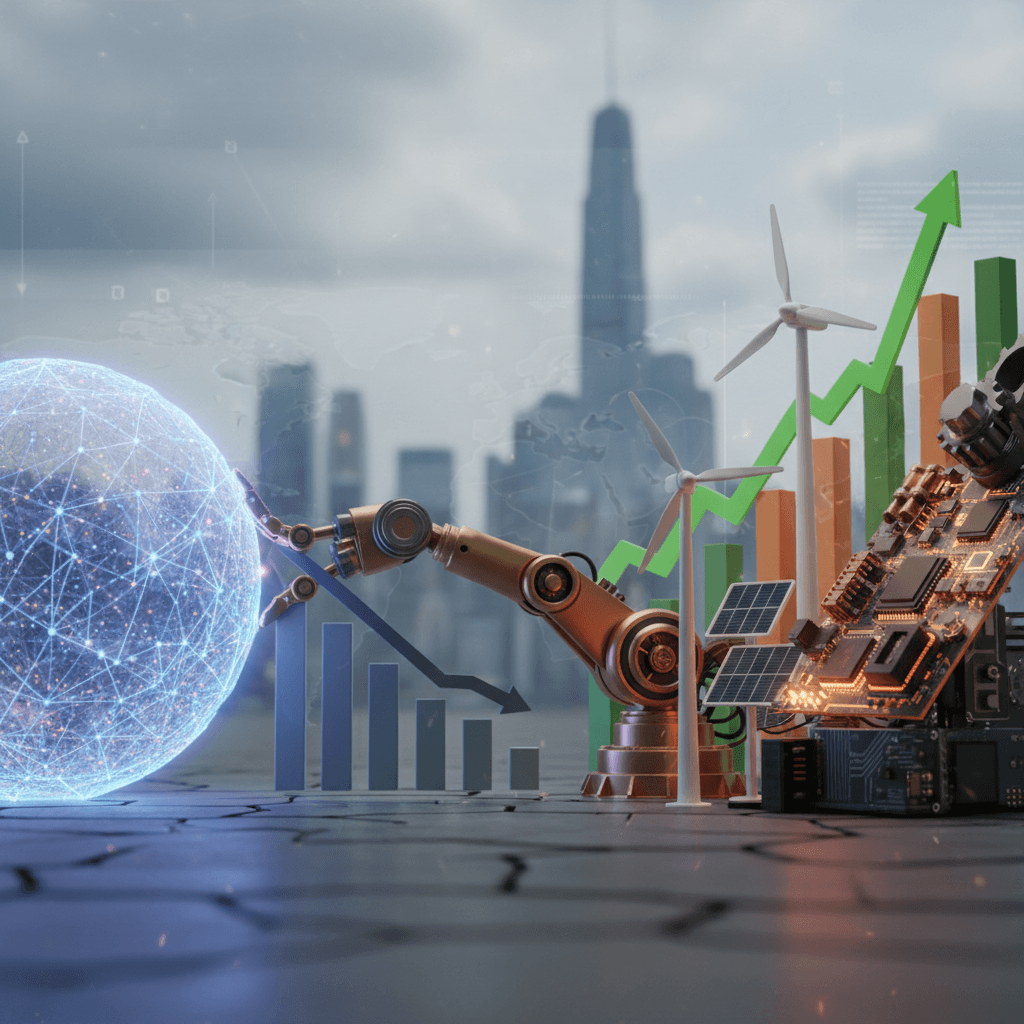

I’ve been looking at the preliminary Q1 2026 numbers, and the trend is stark. While overall funding is down about 15% from this time last year, that drop masks the carnage underneath. Funding for "Generative Enterprise AI"—the darlings of two years ago—has fallen off a cliff, down an estimated 40% from the previous quarter. Meanwhile, investment in what the industry is calling "Hard Tech" or "Deep Tech" is surging. We’re talking robotics, advanced manufacturing, new energy sources, and synthetic biology. These sectors are up a collective 35% year-over-year.

This isn't a correction. It’s a realignment driven by two very real, very un-virtual forces: geopolitics and government cash.

How Does Venture Capital Work in This New Environment?

For years, the venture capital model was about finding a technological edge and a massive Total Addressable Market (TAM). Today, it’s about finding a government subsidy and a defensible supply chain. The game has fundamentally changed.

VCs are now chasing the tidal wave of public money unleashed by legislation like the U.S. Inflation Reduction Act and the CHIPS and Science Act. These aren't small grants; they are nation-building-level firehoses of capital aimed squarely at onshoring manufacturing, securing energy independence, and competing with China. According to a recent analysis by the Brookings Institution, government-related incentives for these sectors now represent a multi-trillion-dollar opportunity over the next decade.