Your $9 Latte Is an Economic Warning Sign

I just paid $8.75 for a flat white in downtown Austin. That’s not a typo. And it’s not some artisanal coffee infused with unicorn tears. It’s just… coffee. And that single, infuriating purchase tells you everything you need to know about the economy in March 2026.

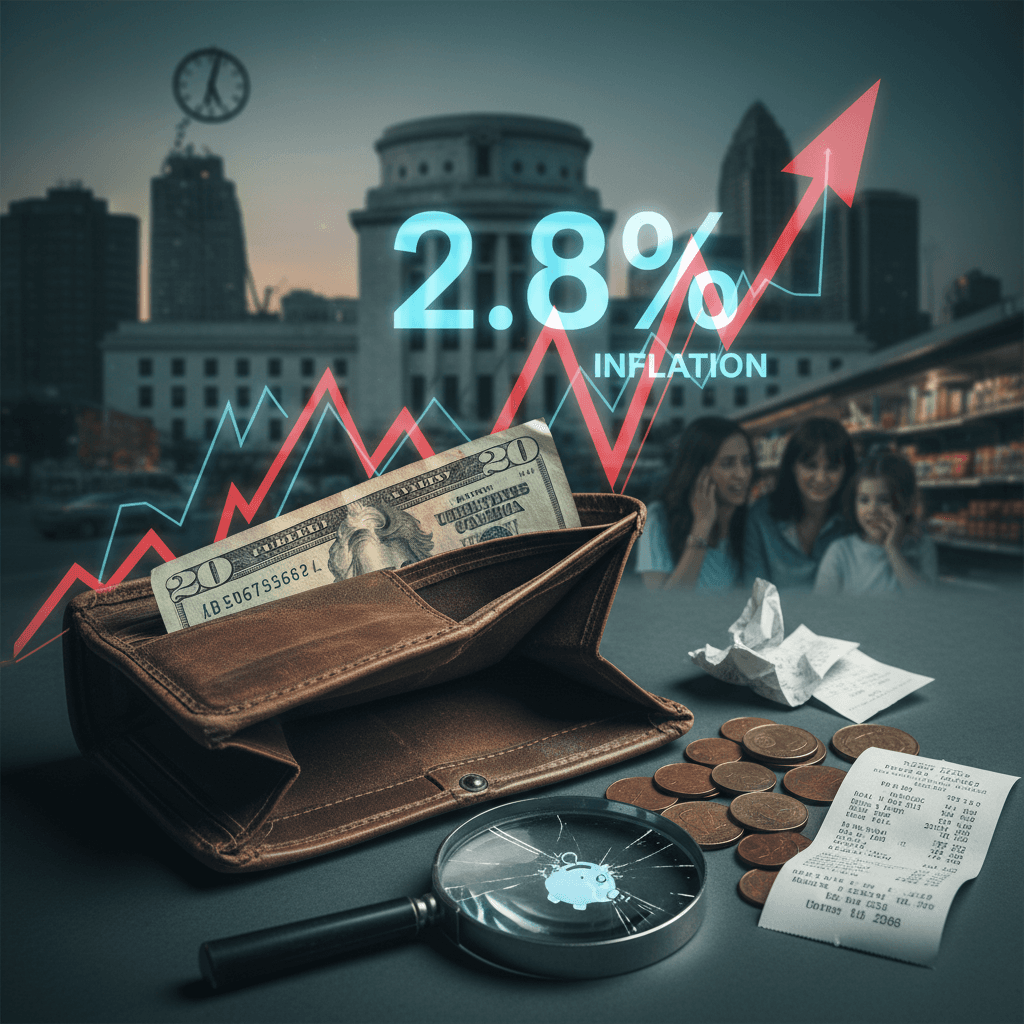

The official numbers, the ones the folks in Washington and on Wall Street wave around, look deceptively calm. The latest Consumer Price Index (CPI) report from the Bureau of Labor Statistics shows year-over-year inflation at 2.8%. A victory, right? The central bankers took their bow, declaring the post-pandemic inflation dragon slain. They popped the champagne back in late 2024 when the number first dipped below 3%.

Don’t fall for it. That 2.8% figure is one of the biggest lies in modern economics. It’s a statistical mirage that hides a brutal reality: for most people, the cost-of-living crisis never ended. It just changed its clothes.

So why does your bank account feel like it's been run through a woodchipper while the experts tell you everything is fine? Because we’re fighting two different inflations. And one of them is winning.

The Great Bifurcation: Goods vs. Services

Remember 2023 and 2024? The easy part of the inflation fight. Supply chains unsnarled. The price of that 70-inch TV you bought on a whim dropped. Used car prices, which had gone completely vertical, finally came back to earth. This was "goods disinflation," and it did most of the heavy lifting to bring that scary 9% inflation number from 2022 down to something more palatable.

The Federal Reserve took a victory lap. But I was telling anyone who would listen back then: popping the goods bubble is simple. The hard part is services. And that’s the bill that’s come due.

Let’s rip open that 2.8% headline number. Here’s what’s really going on under the hood as of March 2026:

- Core Goods CPI: A sleepy -0.5% year-over-year. Your electronics, furniture, and clothes are actually getting a little cheaper.

- Core Services CPI (ex-housing): A blistering 4.1%. This is the monster. This is your car insurance (up 18% YoY, by the way), that haircut, your internet bill, and yes, your $9 coffee.

This isn't a rounding error. It’s a fundamental split in the economy. The things you buy, often made in a factory overseas, are behaving. But the things you do—the services performed by people in your own country—are seeing relentless price hikes. And you can’t outsource a root canal or a plumbing repair.

Why Your Paycheck Buys Less and Less

The Federal Reserve is stuck. Their primary weapon—the federal funds rate, currently sitting at a stubborn 3.75%—is a blunt instrument. It's great at crushing demand for big-ticket items like houses and cars. It’s terrible at stopping your auto insurer from jacking up your premium because replacement parts and skilled labor costs are soaring.

The result? A two-track economy. If you own assets—stocks, real estate—you’ve been fine. The S&P 500 has been grinding higher, buoyed by AI-fueled tech earnings. But if you’re one of the 60% of Americans whose wealth is primarily tied to your salary, you’re falling behind. Wage growth is hovering around 3.5%, which means after you account for services inflation, your real purchasing power for the things you actually need every day is negative.

You’re getting a raise, but your lifestyle is getting downgraded. It’s a silent, insidious tax on living.

The Contrarian Angle: Deglobalization Is Permanent Inflation

Here’s the part the mainstream coverage keeps missing, because it’s politically inconvenient. They’re all still arguing about whether the Fed "did enough." That's the wrong question.