I spent eight years staring at Bloomberg terminals on a Midtown trading floor until my retinas burned. If there is one thing I learned during that decade of watching institutional money move, it is that the market is essentially a manic-depressive entity with a severe gambling addiction. It hears what it wants to hear. It sees pivots where there are only brick walls. And yesterday at 2:00 PM Eastern, the dealer just cut off its credit line.

The financial press is treating the March 2026 Federal Reserve decision as a minor scheduling delay. A slight miscalculation in the timeline. I am looking at the raw data, and I can tell you right now: they are completely missing the plot.

When Chairman Jerome Powell stepped up to the podium and announced that the Federal funds rate would hold steady at 4.50%, you could practically hear the collective gasp from Sand Hill Road to Wall Street. Algorithmic trading bots, which had aggressively priced in a 25-basis-point cut, threw a temper tantrum that wiped roughly $1.2 trillion off the Nasdaq in forty-five minutes.

But the real story isn't the stock market's intraday panic. The real story is why this happened, what it reveals about the true state of the American economy, and exactly how much this is going to cost you by Thanksgiving.

The 2.9% Glitch That Broke the Models

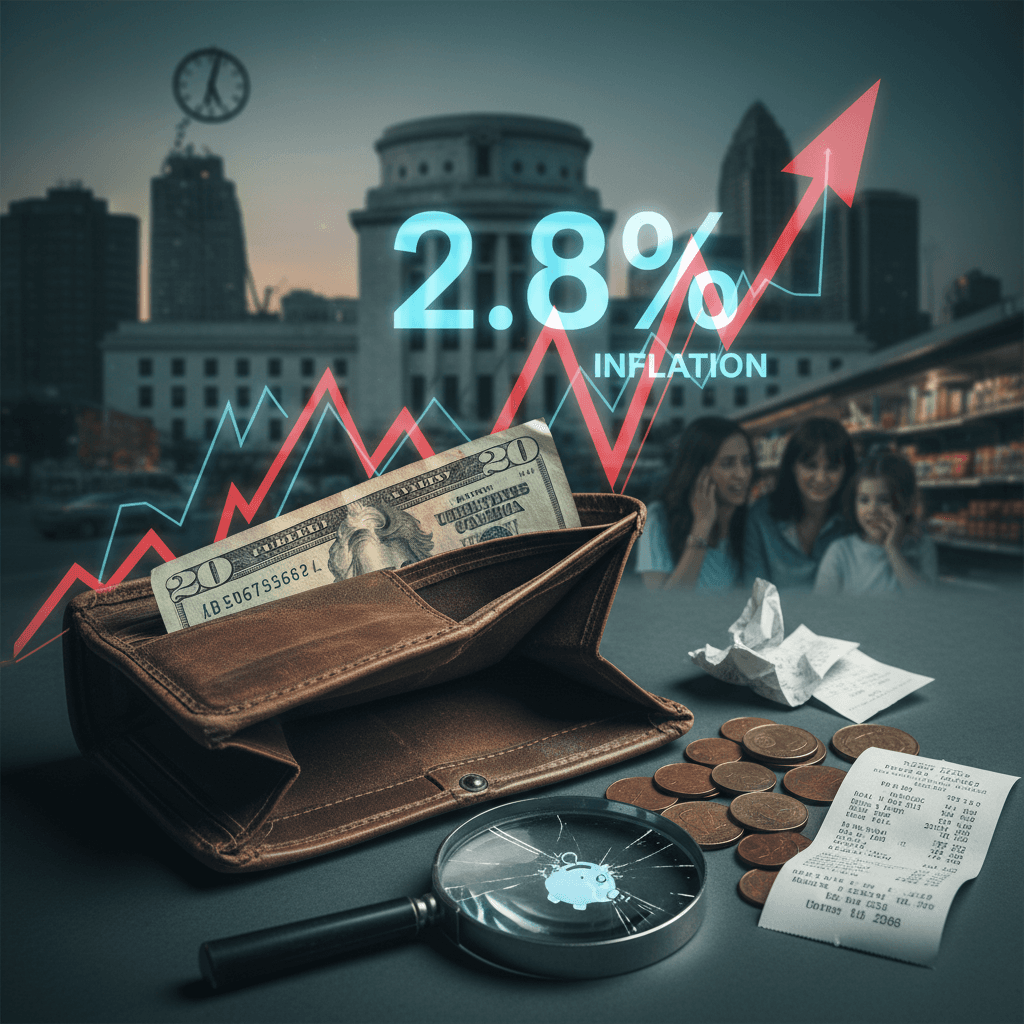

To understand the sheer magnitude of yesterday's decision, you have to look at the math the Fed is staring at. For the last six months, the narrative has been that inflation was defeated. The victory banners were printed. Wall Street analysts were falling over themselves predicting a return to the era of cheap, easy money.

Then the February core Personal Consumption Expenditures (PCE) index dropped.

Core PCE—which strips out volatile food and energy prices—didn't gracefully glide down to the Fed's 2% target. It got stuck at 2.9%. Actually, "stuck" is the wrong word. It dug its heels in and refused to budge. Services inflation, specifically in housing, insurance, and medical care, is running so hot it is melting the thermometers.

Most people look at 2.9% and think, "Close enough, cut the rates." That is a fundamental misunderstanding of central banking. If the Federal Open Market Committee cuts rates while core inflation is stubbornly glued near three percent, they risk reigniting the exact fire they spent the last four years trying to put out. They know that the moment they lower borrowing costs, a tidal wave of sidelined corporate cash will flood the housing and equities markets. Prices would explode overnight.

So they held. And by holding, they just changed the rules of the game for every tech worker, startup founder, and middle-class homebuyer in the country.

Gravity Returns to Silicon Valley

Let's talk about your Restricted Stock Units (RSUs) and why they are suddenly sweating. If you work in the technology sector, your entire compensation package, and arguably your job security, is tethered to a financial concept called Discounted Cash Flow.

Without turning this into a Wharton seminar, here is the brutally simple version: investors value a tech company based on the cash it will theoretically make ten years from now. To figure out what that future money is worth today, they discount it. The interest rate is the gravity in that equation.

When the risk-free rate from the government is near zero, gravity doesn't exist. Startups can float on pure vibes, massive user acquisition costs, and decent pitch decks. But when the risk-free rate is sitting at 4.50%? Gravity is Jupiter-level heavy. A dollar promised in 2036 is practically worthless today if an investor can just buy a Treasury bond and get a guaranteed, risk-free 4.62% yield.

This prolonged high-rate environment is a death sentence for what we call "zombie startups"—companies that don't make actual profit but survive by constantly raising new rounds of venture capital. We're already seeing the cracks. Just look at the capital expenditure required to keep up in the artificial intelligence arms race. As I pointed out recently in The $14B Trap Inside Nvidia's Record Quarter, building large language models requires staggering amounts of hardware. When the cost of borrowing the money to buy those GPUs stays this high, the math for tier-two AI companies simply shatters.

The Contrarian Angle: Powell Wants This Pain

Here is where I diverge from the mainstream consensus you will read on AP News or watch on CNBC.

The media is framing this hawkish hold as a tragedy. They are asking how the Fed could be so blind to the pain in the commercial real estate sector, or the slowing job growth in manufacturing.

My read? Powell isn't blind to the pain. Powell wants the pain.