The entire market held its breath for one word. Just one. And when the Federal Reserve released its statement yesterday, the word was gone.

The word was "vigilant."

For the past 18 months, every single communication from the Fed, the European Central Bank, and the Bank of England has been littered with promises to remain "vigilant" in the fight against inflation. Yesterday, the Fed replaced it with "data-dependent." The S&P 500 immediately jumped 1.2%. Bond yields dipped. The talking heads on TV declared the pivot was finally here. They're all wrong.

This isn't a pivot. It's a trap. And I've seen this movie before back in my Wall Street days. Central bankers aren't signaling victory; they're signaling fatigue. And fatigue is what causes mistakes.

The Long, Grinding Road to 4%

Let’s not forget how we got here. It feels like a decade ago, but it was just 2022 when inflation, peaking at over 9%, was ripping through the global economy. Central banks, led by the Fed, slammed on the brakes, jacking up interest rates at a pace we hadn't seen since the 1980s. They broke things—crypto exchanges, a few regional banks, the IPO market—but they did manage to drag inflation down.

The problem is, they never finished the job. We got stuck in this economic purgatory. The "soft landing" turned into a "no landing," just a long, bumpy cruise at 10,000 feet with the turbulence light permanently on. The market has been pricing in rate cuts for over a year, and for over a year, it's been disappointed. Now, in March 2026, the data shows exactly why the bankers are tired. They’re stuck between a rock and a hard place.

By the Numbers: The Global Stalemate

When I was an analyst, we lived and died by the data dashboard. Narratives are cheap; numbers have consequences. Here’s the dashboard for the U.S. economy right now:

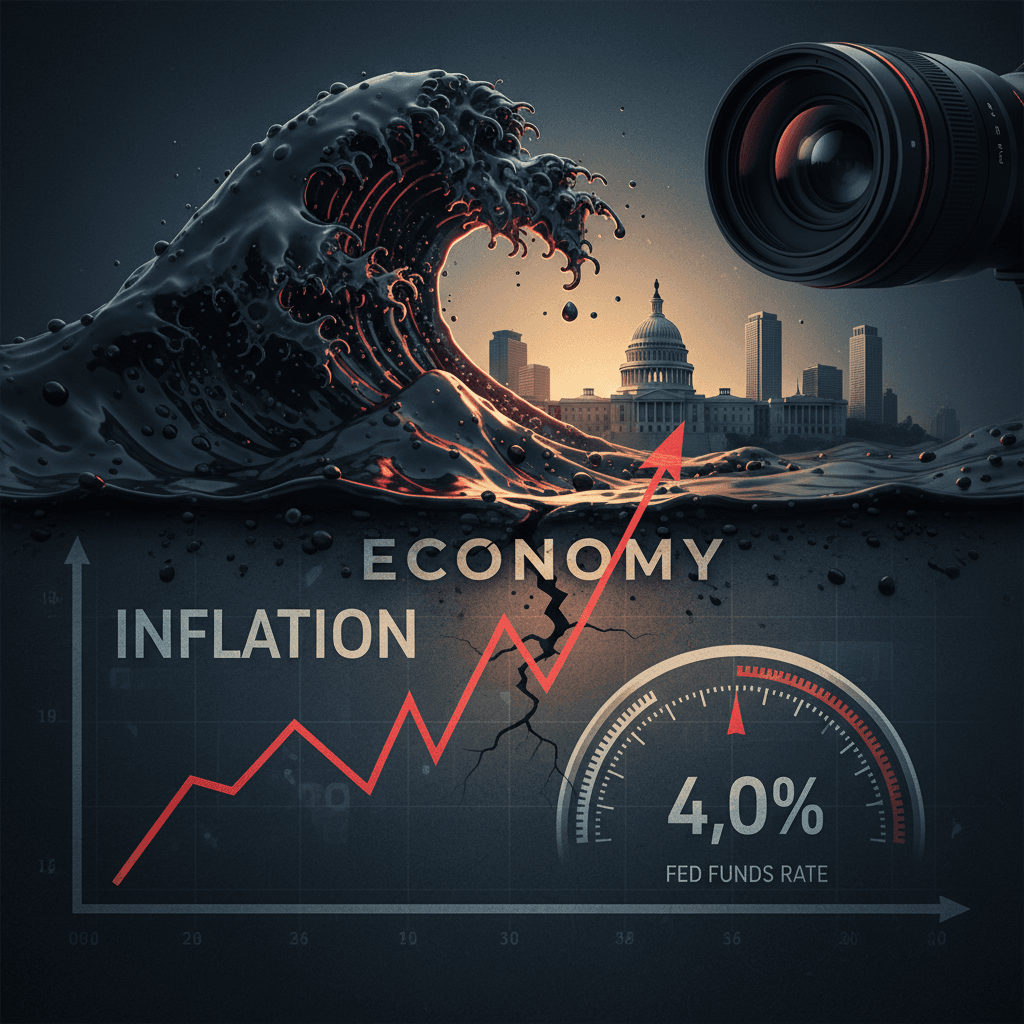

- Federal Funds Rate: 4.0%. It's been here for nine agonizing months. High enough to hurt, but not high enough to kill inflation for good.

- Core CPI Inflation: 2.9%. Stubborn. Sticky. Down from the highs, but nowhere near the 2% target. This is the number that keeps Fed governors up at night, and it's the reason the Fed's March surprise just burned your RSUs.

- Annualized GDP Growth: 1.5%. Anemic. We're not in a recession, but you wouldn't know it from the freight shipping data or the capital expenditure reports.

- Unemployment Rate: 4.2%. Ticking up slowly from the post-pandemic lows of 3.5%. This gives the Fed cover to stay tight, but it shows cracks are forming in the labor market.

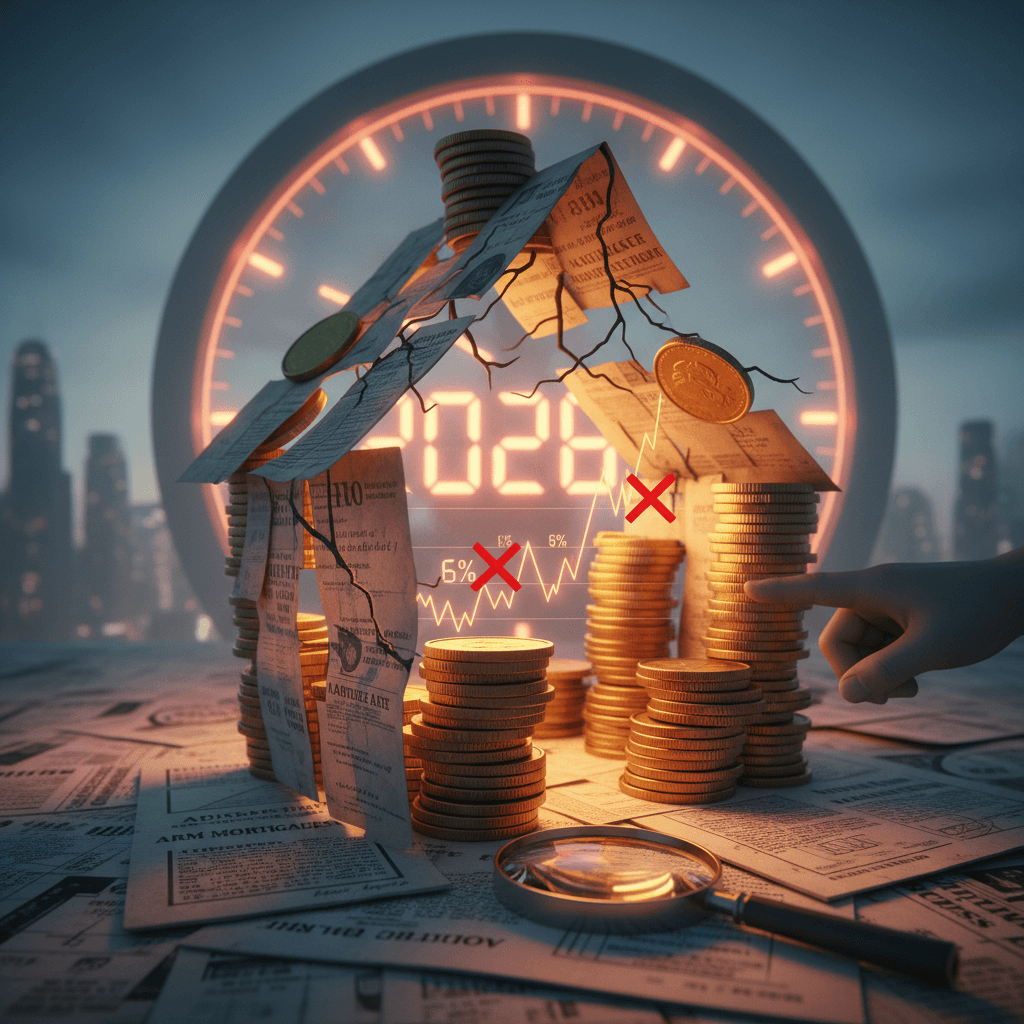

- Average 30-Year Mortgage: 6.8%. This is the real-world impact. It's crushing housing affordability and locking existing homeowners in place, creating a distorted and dangerous market. The idea of a 6% mortgage feels like a distant dream, but even that figure hides some real risks for homeowners in 2026.

This is a portrait of an economy that has absorbed the initial shock of rate hikes but is now slowly being squeezed. The easy gains in the inflation fight are over. Getting from 9% to 3% was the sprint; getting from 3% to 2% is a brutal marathon, and the runners are getting winded.

How do central banks control the money supply and inflation?

This isn't some dark art, though it often feels like it. Central banks have a few primary tools. The most famous is the policy interest rate (like the Fed Funds Rate). By raising this rate, they make it more expensive for commercial banks to borrow from each other overnight, a cost that ripples out and makes loans for cars, houses, and business investment more expensive for everyone. Less borrowing means less spending, which cools down the economy and, theoretically, inflation.